How to Create an Optimal Fantasy Football Portfolio

written by a guy who is legit awful at fantasy

Fantasy Football is like a back-to-school sale. The leaves are beginning to turn, optimism hangs in the air, and as you pick out sweet tye-dye binders and groovy gel pens you can’t help but think “this is going to be my year.” By the end of September your notebooks have unspiraled and your folders are bent. Your pens prove to be as reliable as a supplement Joe Rogan promotes. And someone keeps leaving little deer turd pellets in your gym shoes so that when it’s time to run laps you have to get crap all over your socks and now everybody calls you Dungfoot. It’s like that every year, without fail. But next year can actually, really, be different. What does it take to turn things around? Don’t be a fantasy football player, be a fantasy football investor. Fantasy football is portfolio management. Players are assets, and the goal is to create a portfolio of these assets that outperforms competitors.

Portfolio Management Fundamentals

Building an investment portfolio is all about diversification. Don’t put all your eggs in one basket. Diversification works because the returns of different investments tend to be uncorrelated, like this:

In this scenario, each investment returns either -$5 or +$10 with a 50% probability of each. That’s an average, or expected, return of $2.50. By creating a portfolio that is ½ option A and ½ option B (called Portfolio C), we can get a $2.50 return every single time because the two options are uncorrelated:

Whether or not we diversify, we can still expect $10 return on average. The role of diversification is to reduce risk (not increase return). Diversification makes that $10 return guaranteed. However, diversification can also reduce upside. In this example, portfolio C will never return above $2.50 - it sacrifices upside to remove downside. So why is portfolio C better? Risk aversion. Humans hate uncertainty. Oftentimes investors dismiss risk aversion as irrational, a plague of the unenlightened. But there are real reasons that risk should be avoided where possible.

First is the pain of downside risk. Downside risk is when things go bad. Remember the little squirrel, Scrat, from the Ice Age movies? All he wants is to forage one little acorn, but everytime he gets close catastrophe strikes and he loses everything. In this case, Scrat is investing his best asset (himself) in acorn hunting. The upside risk is that he gets to munch on an acorn but the downside risk is that he gets buried in an avalanche. As is often the case, the downside risk is far more painful than the upside is pleasurable.

Second is that risk is uncertainty, and uncertainty complicates things. Say you’re a master thief planning to steal the Mona Lisa from the Louvre. Things are going well until the security guard you bribed tells you there’s a 30% chance he may not be working the planned night of the heist. Then the getaway driver tells you that he doesn’t work on full moons because he was attacked by a werewolf as a kid. Then the black market buyer you found gets inducted to the French Academy and begins showing signs of patriotic remorse. Alone, each one of these uncertainties is manageable, but taken all at once they doom the heist. That’s because uncertainty compounds. People like to eliminate uncertainty wherever possible because it makes planning - for business and life - much easier.

Risk aversion is covered more on MoneyLemma’s post on paying down debt, but the end result is this:

In most cases, a loss of $10 is more painful than a win of $10. A loss of $100 is more painful than a win of $100. Same for $1,000 and $10,000 and every other number. That’s why good portfolio management optimizes risk-adjusted returns, which takes into account the downside and upside risk. Diversification improves risk-adjusted returns by lowering the amount of risk needed for a given level of return.

Building a Fantasy Football Portfolio

Fantasy football is cool because it allows people who don’t have the talent to play in the NFL, like Tim Tebow, participate in the sport. Fantasy football is not cool because basically everyone loses every year. The stakes for a typical 12-team league are as follows: every team owner contributes money to a prize pool and at the end of the season, the league winner gets all of the prize pool. 11 losers and 1 winner. That means the payoffs look like this:

In investment terms, there’s no gradient for performance. The reward for 3rd place is the same as for 11th place: you lose. If you’re not first, you’re last. This fact inverts the earlier conclusions about diversification. Fantasy players should not diversify. In a normal environment, diversification improves risk-adjusted returns by lowering risk. However, diversification will also reduce upside. In fantasy football, diversification will lower the probability of a low-scoring team but also reduce the probability of a high-scoring team - you would be optimizing for a 4th place finish.

Fantasy players should only be satisfied if their team ends up in the top 8% (the top 1/12th of the league). That’s the only way to make money. Probabilistic scenarios that are positive outliers, like winning fantasy football, are called “the right tail.” The right tail is usually a best-case scenario for investors, like a fire alarm getting pulled during an AP exam. Fantasy players need to maximize the probability of a first-place finish - fantasy is all about getting into the right tail. The way to get an entire portfolio into the right tail is to have a bunch of individual bets pay off at once. That requires correlation, the opposite of diversification. Good fantasy teams need to have all their eggs in one basket! Here’s three ideas of how to do that:

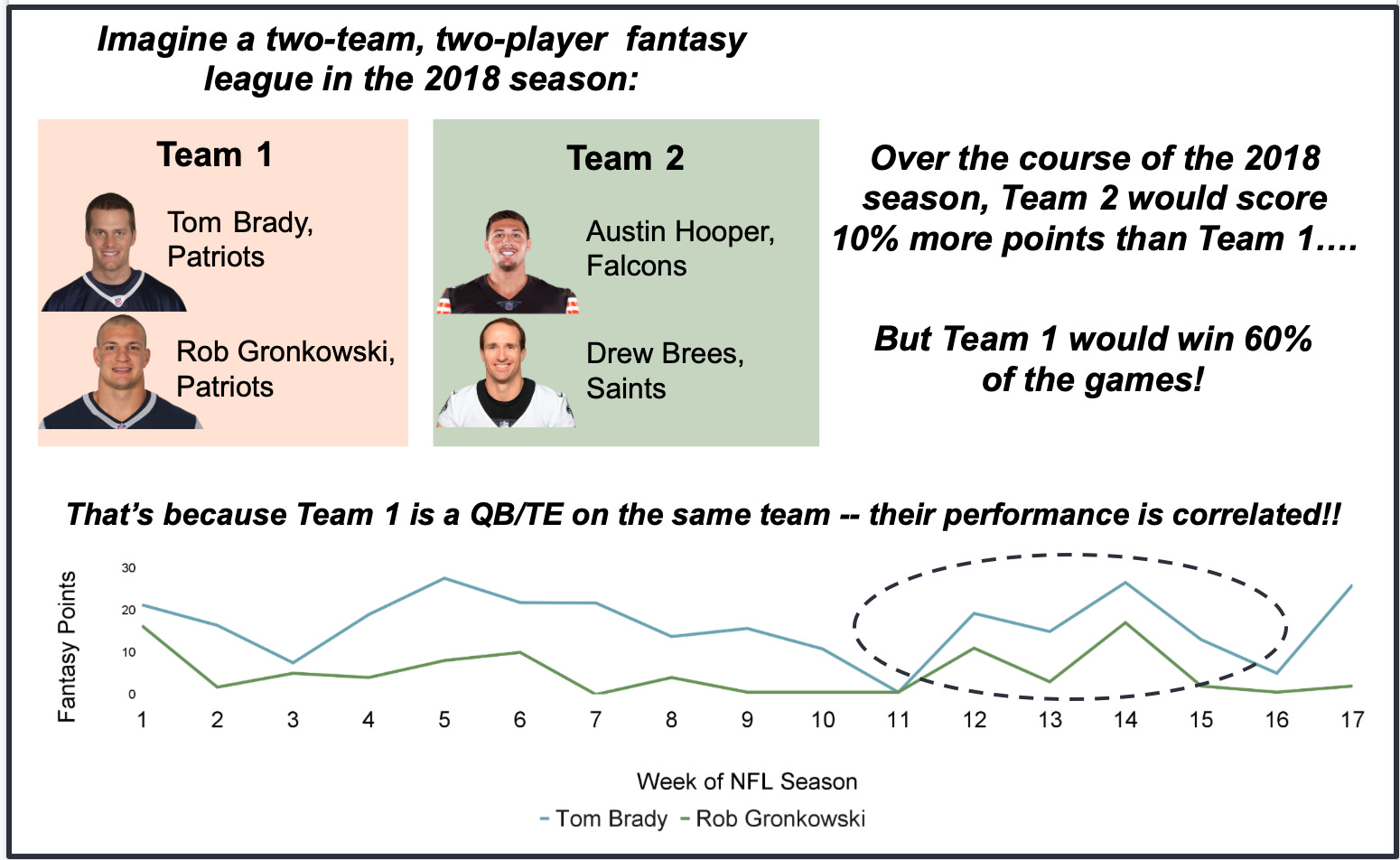

Pick players on the same team, or go all-in on an offense. If a quarterback has a good game, chances are his star wide receiver had one as well. That means a higher chance of a high-scoring week. Here’s an example:

Target high-risk assets: Those players coming off injuries and suspensions, the ones that have “high-ceilings.” The normal rules of investing dictate that risky assets are discounted, and in fantasy that typically holds true. But it shouldn’t:

Adopt a Venture Capital Mindset: Venture Capitalists (what are venture capitalists?) spend more time in the right tail than Henry VIII wive’s spent in guillotines. Venture Capitalists invest in early stage companies, and they are looking for the ~0.01% of all companies that will ever achieve a $1 billion valuation. That requires some serious right-tail thinking.

Y Combinator is one of the most successful venture capital investment funds ever. Their website lists all of the investments they’ve ever made. Many rational investors would flip through that list and laugh. At-home MRI machines, sandwich-making robots, an app that fights parking tickets, smart dishwashers fueled by coal (I made that last one up). These are ideas that have a 99% chance of failing. To a normal investor, those are bad odds. But to a VC investor, 1% chance of success is great if that success is big, fat, right-tail success. The majority of Y Combinator companies fail, but the successes include Airbnb, Doordash, Stripe, Instacart, and a bunch of other investments that have been so lucrative that they could cover the losses of a million failures. Fantasy football managers can learn from this: what many people mistake for a bad investment can be an opportunity for those who understand the fundamentals of risk and reward.

What fantasy football can teach us about investing

Fantasy football is a great example of how blindly following oversimplified advice, like “always diversify” can lead to poor results. Smart portfolio managers optimize for risk-adjusted returns by understanding the fundamental drivers of success in their portfolio.

Go birds. 🦅

Further Reading

https://core.ac.uk/download/84312418.pdf

http://www.columbia.edu/~mh2078/DFS_Revision_1_May2019.pdf