How to ruin a hobby

How card collecting became an asset class

How to ruin a hobby

If you ask the internet, the card collecting hobby has been ruined.

If you look at the numbers, its never been better. Card Ladders reported that August 2025 was a record month for resales with over $400mil in value across 6mil transactions. New card sales are strong too. Target and Walmart sold over $1bil in 2025 and Ebay logged $2.6b in used sales. Altogether sales of sports and trading cards are a ~$20bil market, almost double what they were in 2019 and nearly the size of the global box office.

Card collecting is booming yet passionate hobbyists are saturating the internet with heart-aching requiems for a bygone golden age. For while the market has never been bigger, the hobby is evaporating. Card collecting is no longer a casual pursuit. A single pack of collectible NBA or Pokemon cards starts at $8 and runs much, much higher. That’s if you can even find the stuff. Scalpers painstakingly scout retailers for restockings of any valuable packs, razing the shelves like maggots cleaning flesh off a carcass. Filling an old-fashioned binder with collectible cards costs hundreds of dollars. Collecting used cards has changed too. Once, casual collectors could find valuable used cards in musty boxes at garage sales or thrift shops. Now rare cards find their way to Ebay. If they do end up at a garage sale, rest assured professionals or semi-professionals will aggressively crowd out any casuals. And of course, prices of individual rare cards have appreciated 2x, 5x, 10x, and often 100x in the last decade.

Gone are the days of schoolkids innocently swapping their heroes on the blacktop. Actually, that’s not true. There are still cheaper cards available. Low-tier, mass produced cards that have no possibility of retaining any value. Those aren’t collectibles. For anyone who wants to collect cards, who wants even a long-shot at owning paper worth more than the paper paid for it, there is no entry-level tier. The $20bil card industry caters almost exclusively to high spenders. Who are the big spenders? Serious collectors, compulsive gamblers, professional investors, and social-media crazed speculators. Anyone with deep pockets and a willingness to empty them. In other words, card collecting is not a hobby, it’s an asset class. An asset class with a liquid and efficient market.

The transformation of the card collecting hobby into a bonafide asset class was a conscious effort that began with intellectual property (IP) owners. That includes the major sport leagues, Hasbro (owner of Magic the Gathering), Shueisha (Yu-Gi-Oh) and The Pokemon Company. Every new card sold is sanctioned via licenses granted by the IP owners. These IP owners paid close attention as card collecting became more and more popular throughout the 2000s. Once an afterthought, IP owners have come to appreciate trading cards, particularly the collectibility of trading cards, as serious media assets and avenues for fan engagement. Sports cards are the best example. Within the last five years major sports leagues (NFL, MLB, NBA) have granted exclusive trading card licenses to Fanatics (the same Fanatics that operate exclusive merchandise licenses for many leagues). Fanatics in turn acquired Topps, a leading card brand. Competing sport card brands like Panini or Upper Deck have struggled to stay relevant without key sport licenses.

Consolidating licenses is good business sense. Card collecting as a trend ebbs and flows. In the late 1990s card collecting became a frenzy and competing suppliers responded by printing excessive amounts of cards, tapping into crazed demand. The entire industry was caught up in a bubble. When the bubble burst and demand softened, the world was awash in worthless cards. It almost destroyed the industry. To this day cards from the ‘90s era sell at a steep discount, even typically valuable ones like Rookie cards, because of their overabundance. Collectors call this the “Junk Wax Era".

For sports leagues, the solution to the Junk Wax problem was a sole exclusive license. Fanatics operates on long-term licenses (10 or 20 years with renewal options), incentivizing and empowering them to match supply with demand in a way that optimizes the long-term health of the asset class. The other major trading card brands (Pokemon, Yu-Gi-Oh) have similarly gotten much more sophisticated about supply.

The distribution of cards has changed too. Collectible cards used to be sold everywhere. Convenience stores, grocery stores, newsstands, drugstores, mall kiosks, even Dollar General. Those places still sell low-tier cards, but not collectible ones. Collectible cards (also called hobby decks) are sold through three main channels: breakers, hobby shops, and big-box retailers.

Breakers are collectors who open new packs (and cases of packs), sometimes on a live-stream, and sell off the valuable cards individually. Many collectors are only interested in their favorite teams or players. Breakers can arbitrage risk by opening, say, a $10,000 case of NBA cards, assembling team packs (like all Lakers) and selling those packs to collectors. Many breakers are influencers who amplify popularity and interest in trading cards. Popular breakers swallow huge numbers of packs. Single livestream sessions can burn through hundreds or thousands. Fanatics owns Fanatics Live and Fanatics Connect, streaming platforms for breakers, which means they can keep the breaking economy in a closed loop.

Hobby Shops are another avenue for new card packs. These shops are mainly run by true fans dedicated to spreading passion for card game collecting and playing (yes, people still play the card games). However, Hobby Shops are being increasingly marginalized as a distribution channel. They can’t move the volume of big-box retailers and don’t attract as much attention as breakers. Watch five hobby shop collectors discuss how their access to collectible packs has waned over time:

Big-box retailers sell at scale. Card brands have excised the long tail of retail partners in favor of mega-retailers like Target or Walmart because those retailers can move huge volumes of product efficiently. These retailers mostly stock non-collectible, low-tier cards targeting kids. When they do get the higher-value packs collectors chase, it can cause a riot:

All this means that in the new era of trading cards, sales are bifurcated into two buckets: collectible (hobby) and non-collectible (retail). Retail cards are lower-price and mass-produced. Great for kids or people playing the actual card games, but lacking the one quality collectors desire (scarcity). Retail cards are primarily sold through big-box or general retailers.

The real meat of the $20bil market value of trading cards is in the hobby cards. These collectible cards are ones produced in smaller volumes and sold at higher prices. There’s no public data on this, but a lot of industry insiders seem to think breakers are getting >60% of collectible cards. Hobby retailers get most of the remaining allocation of valuable cards but any regular consumers have to compete with scalpers. Scalpers buy packs and resell at a markup online, or they operate as small-time breakers.

Ten years ago a card hobbyist could acquire a respectable collection through buying $3 card packs at local retailers. Building a hobby collection meant buying those packs, opening them, pulling out the rare cards, and putting them in a binder. Building a collection that way is now all but impossible. Hobby cards, the scarce ones collectors desire, mostly end up in the hands of breakers & scalpers. Not until those cards are unboxed and sold as individuals on resale sites are they accessible to casuals. On resale sites these cards fetch their market value.

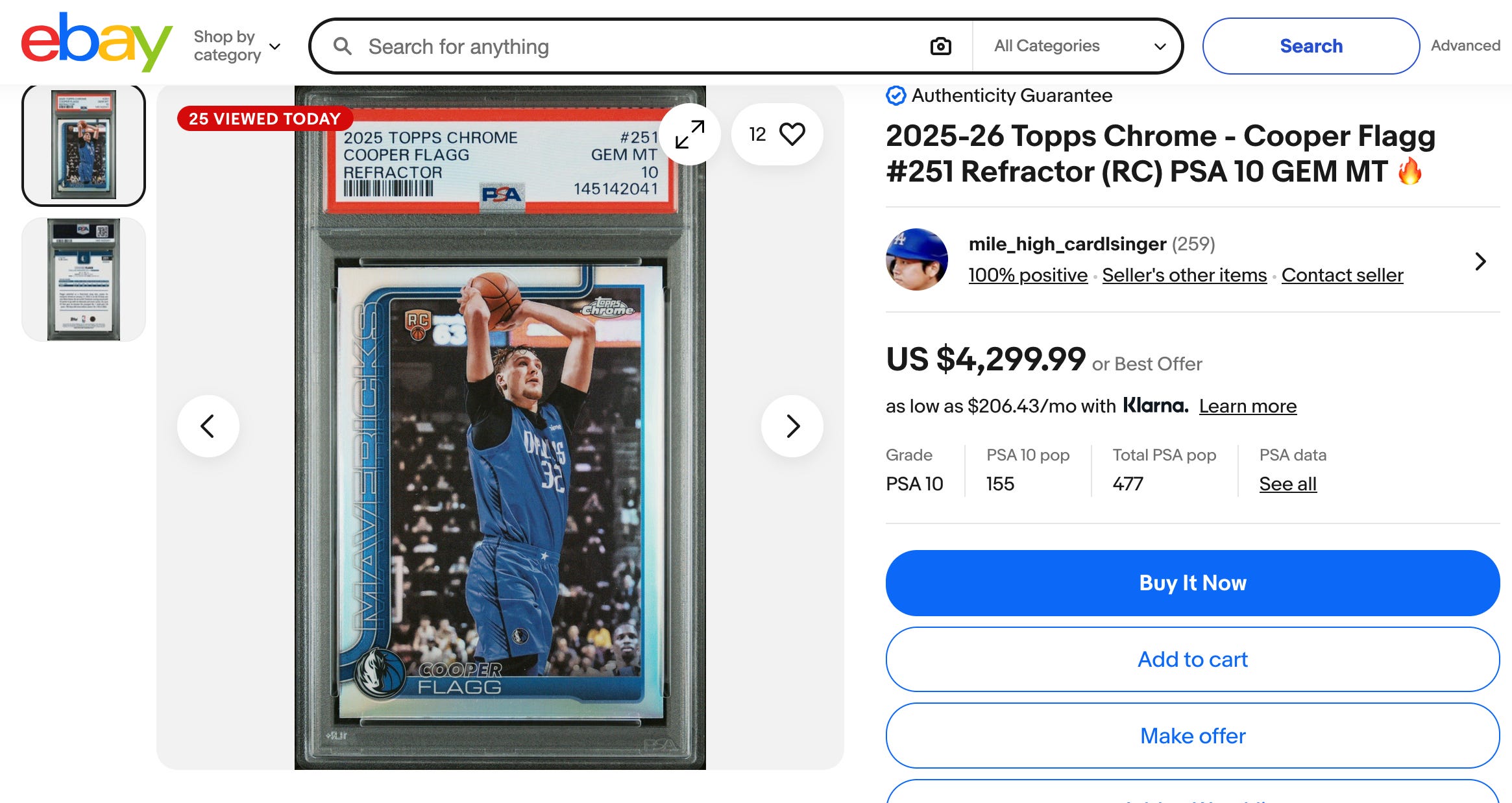

No more can casuals can’t buy a $3 pack and hope to luck out on a $4,000 Cooper Flagg rookie card. They can either buy the card outright for $4,000 or pay a scalper over $100 for that pack. On my math, at $100 a pack, hobby cards have worse expected return than lotto tickets.

The entire collector card ecosystem is now geared to people willing to spend way more on cards. That means amateurs have been cut out in favor of:

Influencers or aspiring influencers for whom pricey cards are a cost of business

Serious collectors willing to invest the time and money to build their collections

Speculators who buy cards expecting the value to go up (maybe because the athlete performs well or because the character gets more popular).

Gamblers who are irrationally wasting money on packs (think scratch-offs)

Institutional investors who have raised serious amounts of money to invest in cards as an asset class

There’s one last leg to this ecosystem, and that is the resale market. Card collecting does not work without a healthy resale market. Here, too, there are signs of a hobby maturing into an asset class.

First, the resale platforms. Ebay has always been the largest marketplace for selling cards. Ebay fees on trading cards have moved from 10% in the mid-2010s to 15% or higher today, which have squeezed hobbyists. More recently other platforms, especially ones that specialize in live-streamed breaking, have emerged. The main two are Whatnot and Fanatics Live. Both have lower fees than Ebay but only allowed verified sellers. A hobbyist cannot realistically sell their collection on these platforms. Again, the casual is squeezed.

Second is card shows. Over 100,000 collectors swarmed Rosemont, IL for last year’s NSCC convention. Trading, comparing, buying, selling, and otherwise talking shop.

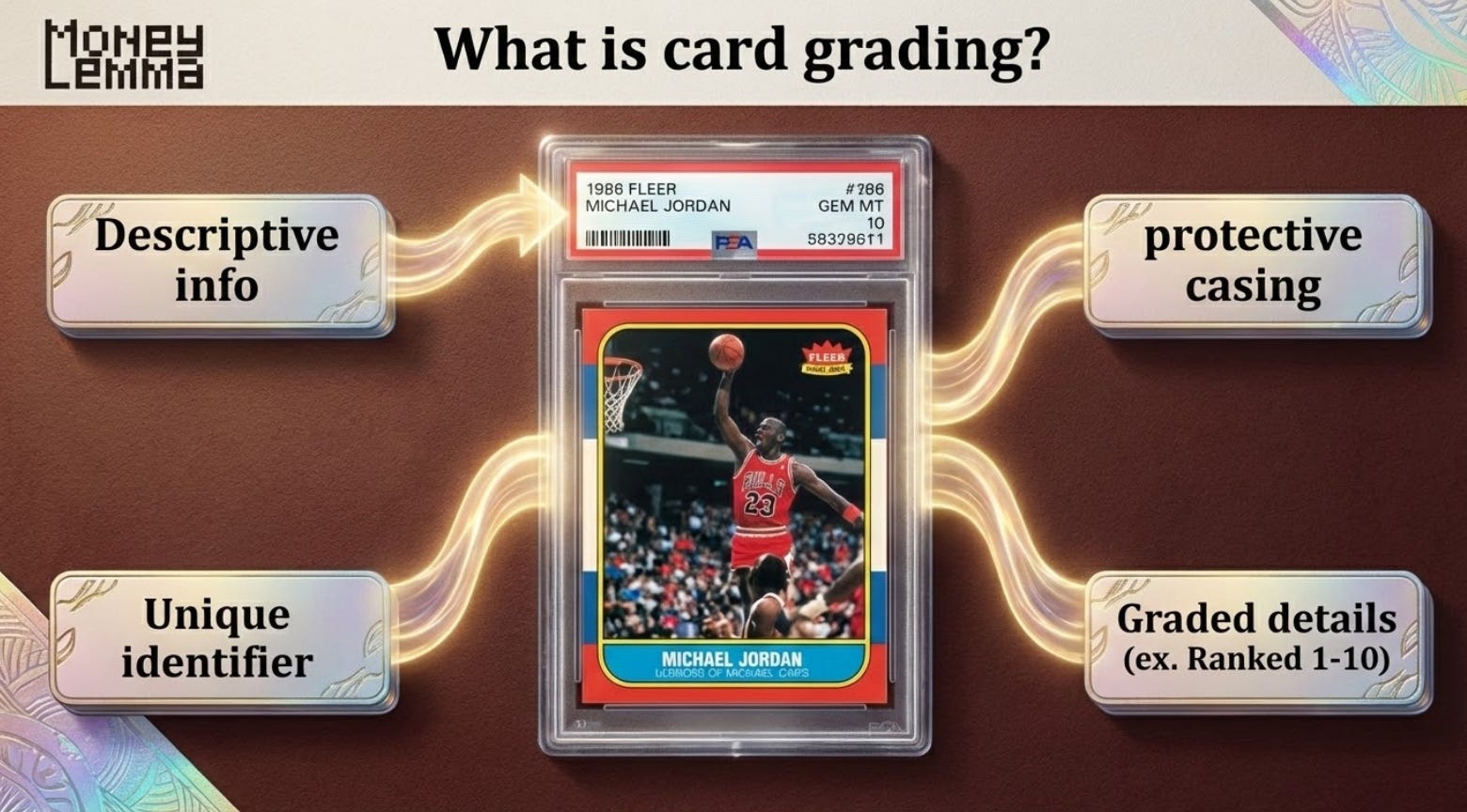

Then there is the grading industry. Any efficient market needs a way to reduce counterparty risk, authenticate assets, and standardize securities for comparability. Grading firms do just that. Owners ship their cards to graders and receive a numerical quality grade and a unique authentication ID.

Grading is a huge business. PSA, the P/E backed industry leader, grades over 15 million cards per year (likely a $1bil+ revenue business). Ungraded cards, lacking verifiability, can trade at a >60% discount to their graded counterparts. In other words, anyone who wants to sell their valuable card needs grading. The problem is that grading has gotten expensive. Collectors Universe, which owns PSA, now controls ~80% of the grading market after acquiring two competitors. PSA has increased pricing 40% since 2019 (or more depending how restructured pricing tiers are accounted for). Cards now cost a minimum of $22 to grade.

While grading is great for transparency and trust, its cost has squashed the low-end of the collectors range. Say a casual collector finds a card worth $30 graded. Grading costs $22 and Ebay fees will cost another $5. All of the value is extracted by these third-parties. Instead, the collector can sell the card ungraded at a steep discount and net a few dollars. The ungraded world is the wild west, rife with fraud on both the buyer and seller side. The value is on the graded cards, and given the economics of grading, that means cards above $50 and often much, much higher. Again, this means that casual and amateur participants are crowded out of the market in favor of those with deeper pockets looking to buy big-ticket cards.

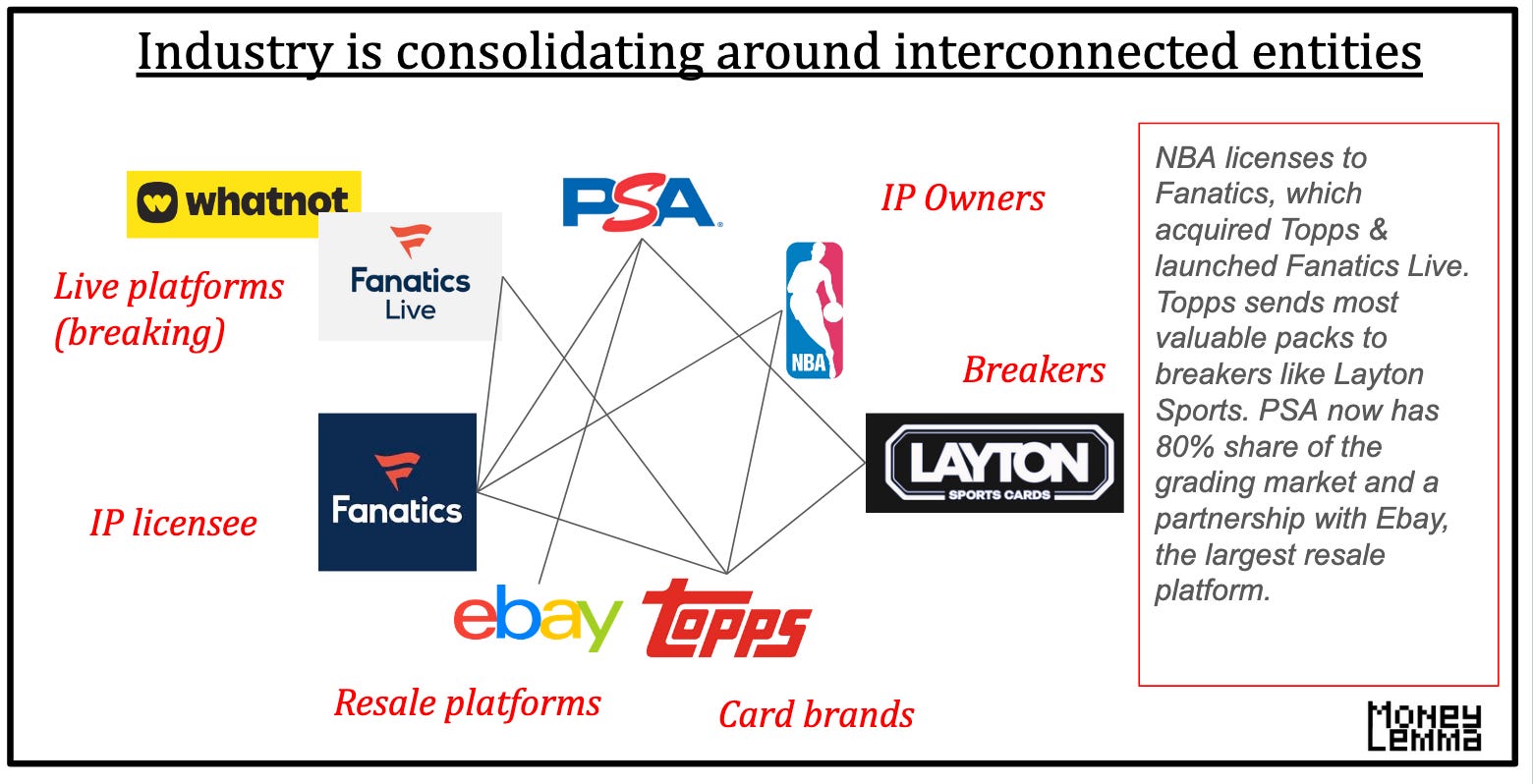

That is how the trading cards industry formalized. What was once a casual, fragmented hobby grew into a large market. Large markets attract serious commercial interests. IP owners (ex. NBA), major retailers (Walmart), private-equity (PSA, Whatnot), large corporates (Fanatics), all realizing the value of sports cards, invested heavily in consolidating key nodes of the value chain. These parties then cooperated to restructure the industry to their own benefit. For example, see how interconnected the big players in the NBA trading card market are:

Industry leaders, the ones consolidating and formalizing the card collecting hobby, are webbed together through a series of formal and informal partnerships. They clearly share a vision for what card collecting should be (and who should profit), and are working together to enact that vision.

These changes have brought positives and negatives. Of course it benefits the entities who engineered it. The parent of grading company PSA. Collectors Universe, for example, reported <$100mil in revenue in its 2019 filing, and today likely makes >$1bil in revenue. Some market participants, too, may benefit. Long-time collectors have seen their portfolios skyrocket in value. A Wayne Gretzky O-Pee-Chee rookie card that sold for ~$20,000 in the early 2010s now fetches $2mil at auction. There’s also much greater transparency and liquidity in the market, which should (theoretically) reduce levels of fraud. Undeniably, though, the hobby of sports card collecting is on its last leg. There’s no room in the market for a casual hobbyist. Card collecting has been professionalized; it’s too expensive and risky for a hobbyist. There are still passionate collectors trafficking in low-cost cards for the love of the game. And there are still groups of friends gathering at hobby shops to actually play Pokemon, Magic the Gathering and Yu-Gi-Oh card games. But the industry has moved on, focused on supply and demand and maximizing expected return. What was once a hobby is now an asset class.

The formalization of sports cards echoes a broader trend across popular media. Over the last few decades corporates and investors have come to appreciate the value of strong IP and dedicated fandom. Again and again, across different industries, business-minded leaders have assumed control of popular media and increased their financial value. Disney bought LucasFilm for $4bil, began cranking out new movies, and easily made its money back on box office alone (let alone the merchandise). Sports teams have gone up in value >10x this decade, according to Forbes, in large part because they’ve become much more professional in how they manage their business. Savvy international expansion, centralized media rights, data-driven front offices, and smarter licensing deals (like in sports cards) are all examples. Other collectible IPs, like sneakers, have gone the way of sports cards. Then there’s Harry Potter, Marvel, Lego, and an endless list of valuable IPs that have industrialized in their own way. In almost every case IP management has been professionalized and formalized. The financial results have been stellar. By many metrics, fans are more invested than ever. And yet, something is slipping away. It’s harder than ever to be a fan. It’s more expensive. It’s more crowded. It’s more corporate. At the core of any valuable IP is authentic human connection. That resonance can be magnified, monetized and mimeographed a million times, but it risks wearing away. What happens then? Will that guiding energy of fandom, which seeks authenticity and originality, naturally migrate audiences away from the tired IP and toward new, fresh IP that is not devoid of personality? Will IP that is professionally managed like a stock portfolio be forced to respond by reigniting its creative core or, if it can’t, collapse under the weight of its own greed? Or might incumbent IP have too firm a grip on the commercial landscape? Could there be a soulless future where creative industries are cornered by professionally managed IP owners? IP owners who form an industrial complex that effectively controls all the many paths to fandom: box offices, concert venues, retail merchandise, social media, live streaming. These IPs could flood the world with mediocre, over-monetized content, drowning out any authentically creative projects, and there’d be nothing to stop them. One immense, inane stormcloud, crowding out the competition, raining endless slop on the helpless fandoms of the world. Albeit, at very impressive 30% return on invested capital.